Many motorists have noted, with justifiable concern, that car insurance costs went up by a significant margin in 2016. A closer look at the market trends gives the indication that auto insurance costs have been steadily rising for the last 5 years across the U.S. And...

Important Information Most people will not argue the need to have car insurance for their cars because they know that how important auto insurance is to cover difficult situations such as theft, natural disasters, and accidents. However, what most car-owners don’t...

Many motorists feel car insurance costs are higher than they want to pay. Rates are indeed on the rise. But some folks have taken to telling “white lies” to mislead insurance companies and get lower car insurance rates. A nationwide survey conducted by a leading...

Shoes that are too tight can hurt your feet. Pants that are too loose will fall down. Whatever clothing you’re putting on your body, it’s important to find the right fit if you want to look and feel your best. The same can be said about homeowner’s insurance. If you...

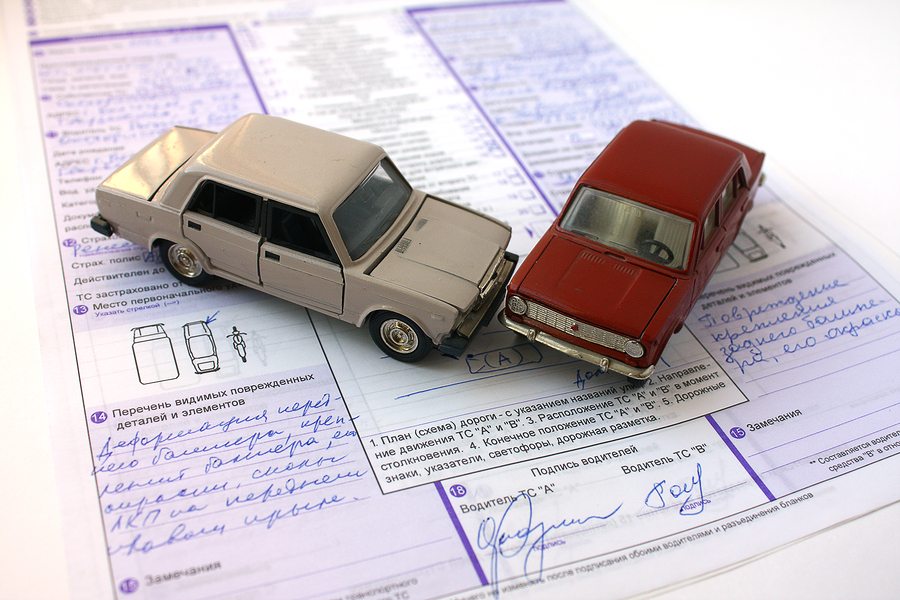

Car accidents happen to new and old drivers alike. Knowing the steps to take following an accident can ease the insurance process and protect drivers from liability. The correct immediate actions can save insurance and personal worries later. These are the steps to...

Homeowners are taking too many risks with insurance coverage. According to a recent study by the National Association of Insurance Commissioners (NAIC), only a small percentage of homeowners plan for natural disasters when updating insurance plans. Approximately 4/5...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site, you agree to accept our cookies.AcceptPrivacy Policy